The land market had its best year in nearly a decade in 2021 as land sales rose 6% and outperformed the pace of acquisitions of other commercial real estate types, according to the 2021 Land Market Report from the REALTORS® Land Institute (RLI)(link is external) and the National Association of REALTORS® (NAR).

Land sales of members of RLI and NAR rose on average by 6% in 2021, the best performance since land sales of members of these associations was collected by surveying the members in 2014. Historically-low mortgage rates in 2021 that drove home sales, the historic net absorption of multifamily and industrial commercial space, and the resiliency of the retail property market arguably drove the demand for land which is the physical foundation for real estate development.

Land Sales Outperform Sales of Commercial Real Estate Properties

The increase in land sales among RLI and NAR members surpassed the increase in dollar sales volume of transactions for commercial real estate properties such as single-family rentals (5%), industrial properties (4%), and apartment buildings (2% Class A and 3% Class B/C). The strong growth in land sales clearly outperformed the decline in transactions of retail, hotel, and office properties of RLI and NAR members in 2021.

Residential and Industrial Land Sales: Hottest Land Markets

By type of land, residential, industrial, and recreational land were the hottest land markets, with REALTORS® reporting an average sales increase of nearly 5% to 7% during the course of 2021. Land prices for office/retail use also rose nearly 4% in 2021 after staying flat on average in 2020. Residential land sales accounted for 59% of all land sales in 2021.

According to NAR’s REALTORS® Confidence Index Survey, a monthly survey of the transactions of members engaged in residential real estate, residential land for the buyer to build on accounted for nearly 4% of the combined sales of residential properties (single-family homes, condominiums, manufactured homes, residential land), up from about 3% in 2020.

As of 2021 Q4, the underlying value of the land of real estate owned by households totaled $15 trillion, up from $13 trillion in 2020 Q4, according to Federal Reserve Board data. NAR estimates that the land value accounts for 40% of household real estate assets after the value of the structure based on replacement value is deducted from the total value of the real estate assets held.

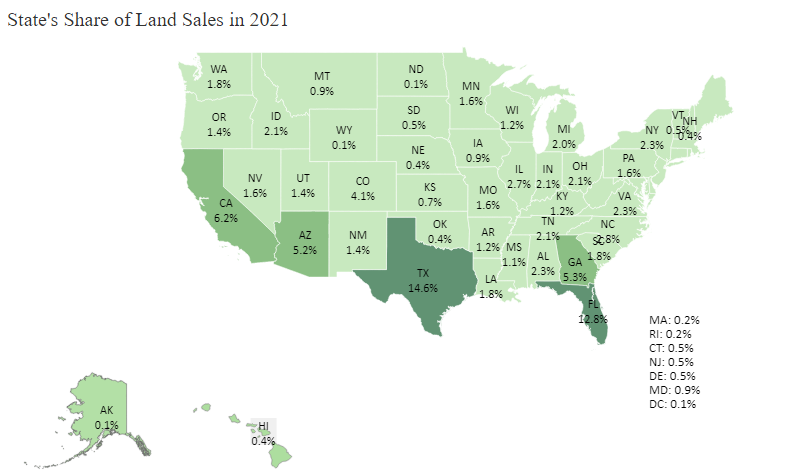

Top 5 Land Markets of REALTORS®: Texas, Florida, California, Georgia, and Arizona

The states with the largest shares of land sales were Texas (15%), Florida (13%), California (6%), Georgia (5%), and Arizona (5%), garnering 44% of land sales in 2021.

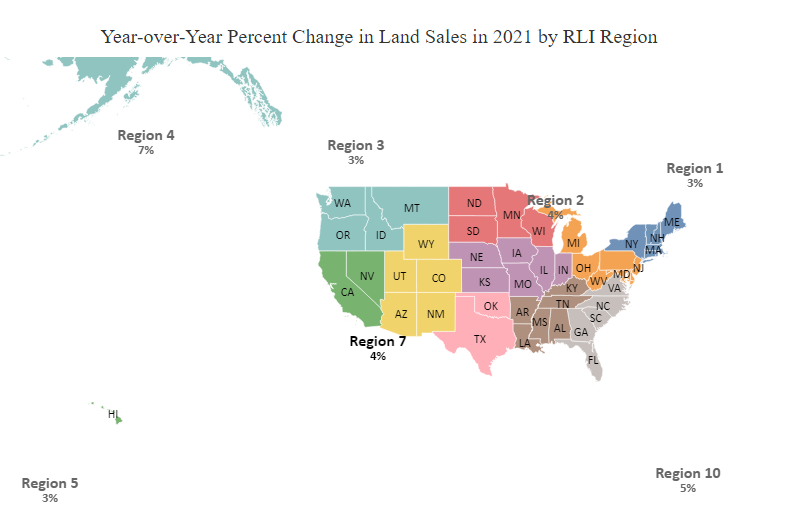

Regions 4, 6, and 8 were the markets with the highest increases in land sales in the range of 7% to 8%, with about 1 in 5 REALTORS® reporting a land sale in 2021.

Not surprisingly, Regions 1 and 10 had the most expensive developed residential lands, at over $250,000 per acre. The next most expensive residential land markets were Regions 6 and 8, at a little over $100,000 per acre. The least expensive markets were Regions 7 and 9 with residential land prices hovering at $15,000 per acre.

Developed residential land typically sold in 60 days but sold in 30 to 45 days in Regions 1, 3, 4, and 5.

Land Market 2022 Outlook

NAR Chief Economist Lawrence Yun noted in the report that he expects 2022 to remain a good year for the land market: “Even with rising interest rates, I expect sustained growth in land sales and prices this year, driven particularly by the demand for multifamily and single-family housing needs. The shift from just-in-time to just-in-case inventory management amid supply chain issues will continue to drive the demand for land for new warehouses. Moreover, agricultural grain prices will remain elevated due to the war in Ukraine and thereby boost demand for farmland.”

REALTORS® reported that the development of residential lots has been hampered by zoning regulations. Fifty percent of REALTORS® reported that zoning regulations have become more difficult in the past five years. The development of residential lots is essential to addressing the housing shortage, with 6.8 million units underbuilt since 2000 as of 2020.

About the Land Market Report

The REALTORS® Land Institute(link is external) defines a land transaction as one in which the value of the land is at least 51% of the value of the transaction.

The REALTORS® Land Market Survey is a collaboration of the REALTORS® Land Institute (RLI) and the National Association of REALTORS® (NAR) that started in 2014. The objective of this survey is to gather information and insights about the state of the land market based on land transactions of land real estate professionals who are members of NAR and RLI. The information is intended to be a valuable resource for market intelligence and policy advocacy.

To increase the number of respondents and collect timely information about land transactions during the year, land market questions were integrated into the Commercial Real Estate Quarterly Market Survey (CREQMS) and the monthly REALTORS® Confidence Index (RCI) Survey. The CREQMS is sent out quarterly to approximately 80,000 commercial members of NAR, which include members of the REALTORS® Land Institute. The monthly RCI Survey was sent out to 50,000 randomly selected members of the NAR whose primary area of business is residential. There were 31,335 respondents to these two surveys, of which 562 respondents (could be the same respondent across months or quarters) reported a land sale. Thus, estimates such as the year-over-year percent change in sales and prices are the average of the monthly or quarterly figures reported by the respondents

.